Bridge Over Troubled Fiscal Waters?

Only if Federal Aid Is Used Wisely

Introduction

As New York City enters the second year for the pandemic-wracked economy, its Fiscal Year 2022 Preliminary Budget once again closes budget gaps primarily with short-term solutions. The federal American Rescue Plan presents an opportunity to put the City’s finances on sound footing, which can help rebuild the thriving metropolis that supports all New Yorkers, especially those in need. However, achieving this goal depends on wise use of federal aid, diligent management focused on delivering quality critical services and increasing the efficiency of operations, so they are fiscally sustainable.

The Preliminary Budget reflected a bleak reality. Despite signs and expectation of a recovery, the pandemic and economic restrictions have decimated parts of the City’s economy and brought many long-standing inequities to the fore. The COVID-19 induced recession has reduced City tax revenues and increased pandemic-related expenses. Most prominently, property taxes are expected to decline an historically significant 4.3 percent after years of consistent growth averaging 6.2 percent annually, even during the last two recessions.1 The pandemic has battered the City’s commercial real estate market and will depress property tax revenue growth throughout the financial plan’s four years. Budget gaps for fiscal year 2023 and beyond have widened to over $5 billion annually (including placeholder labor savings), and the City faces great uncertainty about the economic recovery and non-property tax revenues.

The City should seize the opportunity presented by the more than $5 billion in additional federal relief in the American Rescue Plan, along with substantial aid that will directly flow to City residents and businesses, to stabilize its finances both for today and the long run. Essential to success is the prudent use of federal resources: addressing the most pressing pandemic and related expenses, responsibly backfilling shortfalls in tax revenues temporarily, spreading aid over time to provide a glide path for restructuring, and resisting the urge to fund programs with recurring costs.

Rather than proposing forward looking actions that would put the City on a path to solid fiscal footing, Mayor Bill de Blasio’s recent Financial Plan primarily relied on short-term strategies to close near-term gaps. The Executive Financial Plan, expected next month, should include a plan for prudent use of these new resources over multiple years, coupled with a commitment to innovative improvements across City government to increase efficiency and cost-effectiveness, while also improving services critical to the City’s competitiveness and fairness.

Unwise use of federal stimulus funding would leave the next Mayor with an even more daunting fiscal challenge. Likewise, while tax increases are neither proposed nor needed to balance the budget, the Mayor and many vying to be his successor have voiced support for higher taxes on the wealthiest New Yorkers; this infusion of federal aid provides resources more than sufficient to bridge to a stable fiscal future so there should be no need to further consider increasing taxes.

Budget Gaps Widened Since November 2020 Financial Plan

The NYC economy has been reeling from the impact of the COVID-19 pandemic, with massive job losses and high unemployment, declines in tax revenues, and substantial new costs for responding to the public health crisis. The City has used a range of actions to balance its budget during the crisis, including spending reductions, a hiring freeze, debt refinancing, drawdowns of reserves, and already appropriated federal aid.2

In November 2020, the City projected a $3.8 billion gap in fiscal year 2022 and gaps of around $3 billion annually in fiscal years 2023 and 2024. On the positive side, tax revenues had performed better than expected when the budget was adopted last June; personal income tax and business taxes were about $640 million ahead of the plan due to both a nascent recovery and federal aid. Wall Street was experiencing record profits, while significant federal aid flowed to City businesses and residents mainly through the Paycheck Protection Program (PPP) and Unemployment Insurance (UI). Furthermore, through December 2020, the City had regained 31 percent of the more than 874,000 private jobs lost through April 2020; however, the city’s recovery has been slower than the rest of the state and the U.S. due to the severe impact of the pandemic on the leisure and hospitality sector.3

By January 2021, when the Preliminary Financial Plan for Fiscal Year 2022 was released, the situation had worsened. Job gains stagnated with the new wave of infections and restrictions. The tentative property tax assessment roll for fiscal year 2022 decreased the market value of commercial property by 16 percent and residential property over 4 units by 8 percent.4 This $71 billion loss in market value (5.2 percent) is unprecedented in recent history—the last time the City experienced year-over-year declines in market value was in the mid-1990s.

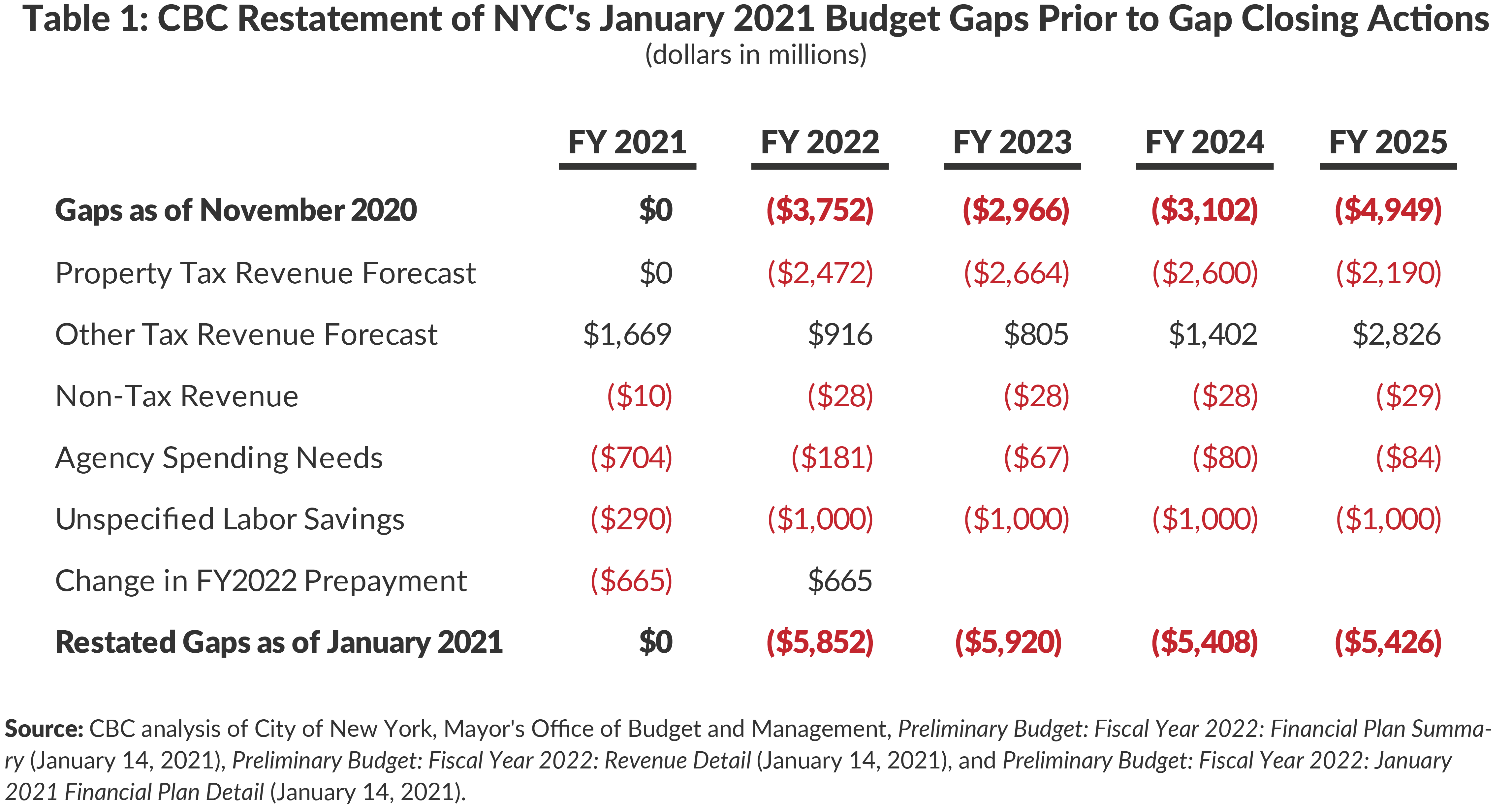

Tax revenues were a mixed bag. For fiscal year 2021, personal income and business taxes continued to outperform forecasts by nearly $1.7 billion. However, this current year forecast increase was almost entirely offset by next year’s forecasted $1.6 billion net decrease, comprised of a $2.5 billion shortfall in property tax revenue due to market value decline and $916 million in higher than projected non-property tax revenues. (See Table 1.) The property tax revenue decrease carries forward into fiscal years 2023 to 2025; the decrease in market values and the anticipated slow recovery for commercial real estate led the City to reduce the property tax revenue forecast by $2.7 billion in fiscal year 2023, $2.6 billion in fiscal year 2024, and $2.2 billion in fiscal year 2025. Non-property taxes are expected to perform better than previously forecasted, though not enough to offset the shortfall in property tax revenue in fiscal years 2023 and 2024.

While tax revenue projections overall were lowered, expenditure projections increased—$704 million in fiscal year 2021, $181 million in fiscal year 2022, and under $100 million per year thereafter. The fiscal year 2021 new needs fall into two large categories. Nearly half of the needs relate to City programs and efforts in response to the pandemic, including $200 million for Test and Trace, $59 million for Learning Bridges, and $52 million for COVID-19 food programs. The balance added funding for ongoing programs, including $220 million for Carter Cases (special education tuition at private schools), $58 million for leases for Department of Education programs, $11 million for a speed camera expansion, and $10 million for Department of Design and Construction costs related to Borough-Based Jails. In fiscal year 2022, the City added $53 million for Fair Fares. One recurring expenditure related to COVID-19 was $35 million in annual funding for academic resiliency programming in fiscal years 2022 to 2025.

Importantly, the $1 billion in unspecified recurring annual labor savings added to the financial plan in June 2020 is still included. In the intervening eight months, the City’s main action to realize this savings was to defer $776 million of payments to City workers from fiscal year 2021 to fiscal year 2022—achieving some of the fiscal year 2021 savings at the cost of widening the fiscal year 2022 gap. There remains $290 million in expected savings in fiscal year 2021 and $1 billion annually in fiscal year 2022 through 2025.5 Absent a concrete and feasible plan that would achieve these savings, they are appropriate to include when representing the City’s budget gaps.

Accounting for these revenue and expense changes, the City needed to close a $5.9 billion gap in fiscal year 2022 in the Preliminary Budget. The fiscal year 2023 to 2025 gaps were $5.9 billion, $5.4 billion, and $5.4 billion, respectively.

Short-term Strategies Fail to Address Long-Term Gaps

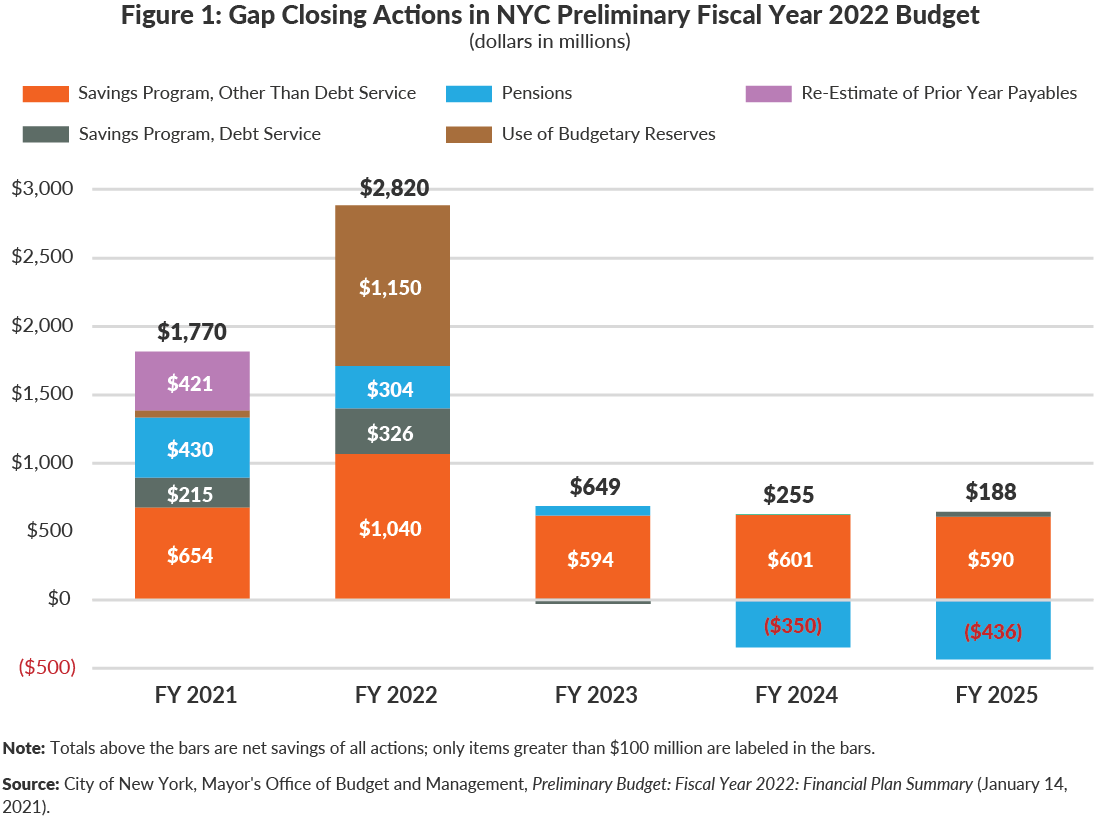

The City’s actions to close the fiscal year 2022 gap consisted largely of one-time resources and front-loaded savings with insufficient recurring value. (See Figure 1). These were comprised of a Citywide Savings Program (CSP), debt service refunding, changes to pension assumptions and methods, use of budgetary reserves, and re-estimates of prior year payables. These provided $1.8 billion in fiscal year 2021 and $2.8 billion in fiscal year 2022, but just $649 million in fiscal year 2023, $255 million in fiscal year 2024, and $188 million in fiscal year 2025. With the unspecified recurring labor savings included, the resulting budget gaps were $1.3 billion in fiscal year 2022, and over $5 billion in each of fiscal years 2023 to 2025.6

Citywide Savings Program

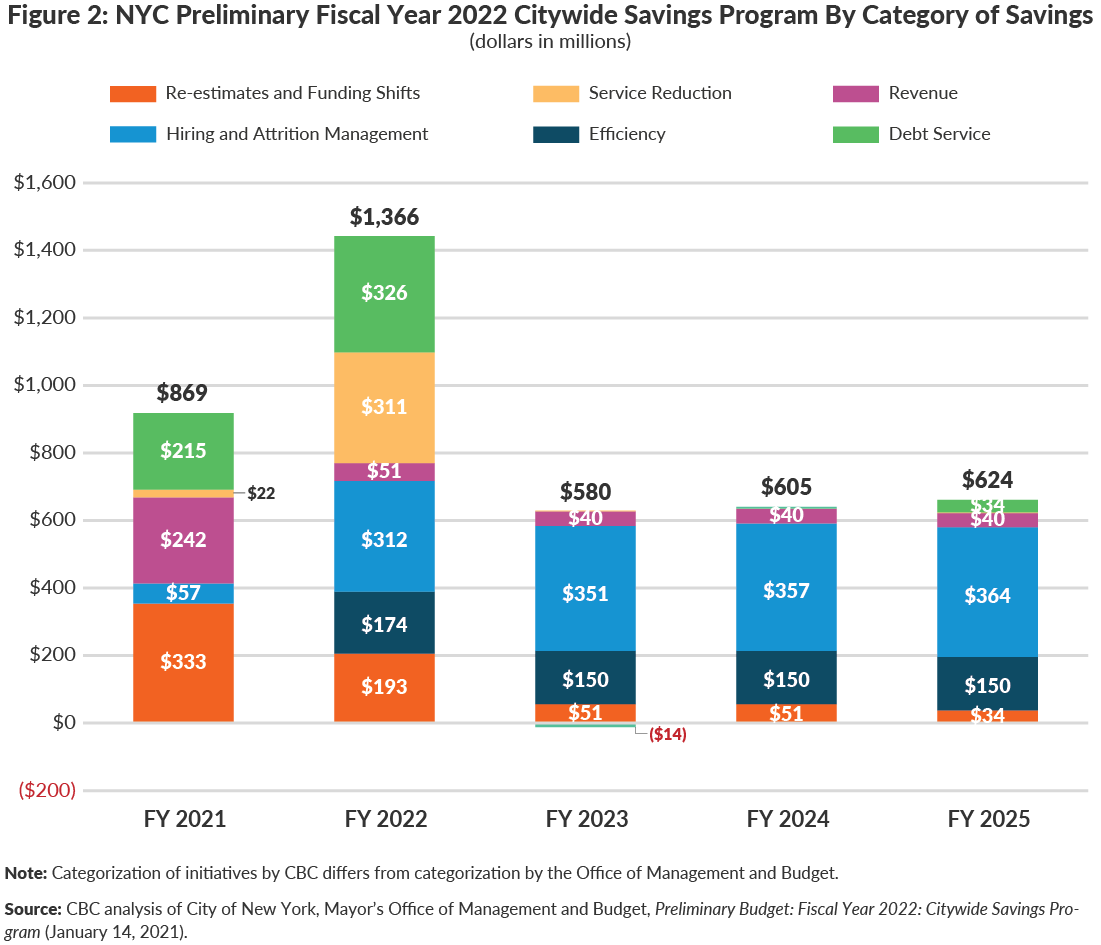

The total CSP provides $2.2 billion in savings across fiscal years 2021 and 2022, with about $600 million recurring annually in fiscal years 2023 to 2025. Excluding debt service savings of $541 million across fiscal year 2021 and 2022, the remaining savings are $1.7 billion in the first two years.7 (See Figure 2).

The largest category of savings in fiscal years 2021 and 2022 is re-estimates and funding shifts, which provided $525 million in savings. Re-estimates of spending and funding shifts to federal or state aid are usually short-term solutions that reduce City-funded spending in the current and upcoming year. The savings program’s re-estimates include initiatives across 18 agencies that reduce other than personal service expenditures by $10.6 million in fiscal years 2021 and 2022. Three social service and health agencies have secured nearly $100 million of one-time federal funding for prior-year expenses.8 The City also secured $100 million in additional Medicaid reimbursement.

Similarly, most of the $311 million in fiscal year 2022 savings from service reductions reflect reduced programming due to the pandemic and are not expected to recur. These include reductions for the City University of New York Accelerated Study in Associate Program (ASAP), Tutor Corps, and Apple Corps; slowdown in supportive housing production; temporary reduction in Fair Student Funding at the Department of Education; and delay in the 3K expansion (the latter two are expected to be restored with federal funding). The City is also implementing a $14.6 million one-time reduction in subsidies to libraries.

Conversely, efficiency savings and hiring and attrition management are two types of savings that should recur. The first provides about $174 million next year and $150 million in fiscal years 2023 to 2025, mainly from reduced overtime at the Police Department and Department of Correction, though the City has had difficulty in the past controlling this spending. Hiring and attrition management savings are realized by reducing the non-safety headcount at City agencies by limiting new hires. The City’s hiring freeze now allows agencies to replace just one for every three vacancies in some functions; previously agencies were permitted to replace one of every two vacancies.9 The City expects to save $57 million this year and about $350 million annually thereafter. Importantly, the City has reduced headcount 5,112 in the outyears—a welcome change.

The City also is implementing revenue initiatives expected to generate about $242 million this year, $51 million next year, and $40 million annually thereafter. Revenues expected in fiscal years 2021 and 2022 include revenue from reimbursement from New York City Health + Hospitals, higher reimbursement for ambulances, landfill closure revenue from methane gas, and affirmative litigation revenue at the Law Department. The Department of Finance is expecting recurring revenue beginning in fiscal year 2022 from two initiatives related to property assessments: use of LIDAR data capture to support property tax assessments, and assessment of a new class of property referred to as revocable consents, which are found under streets, sidewalks and public areas and administered by Department of Transportation.10

Debt Service Savings

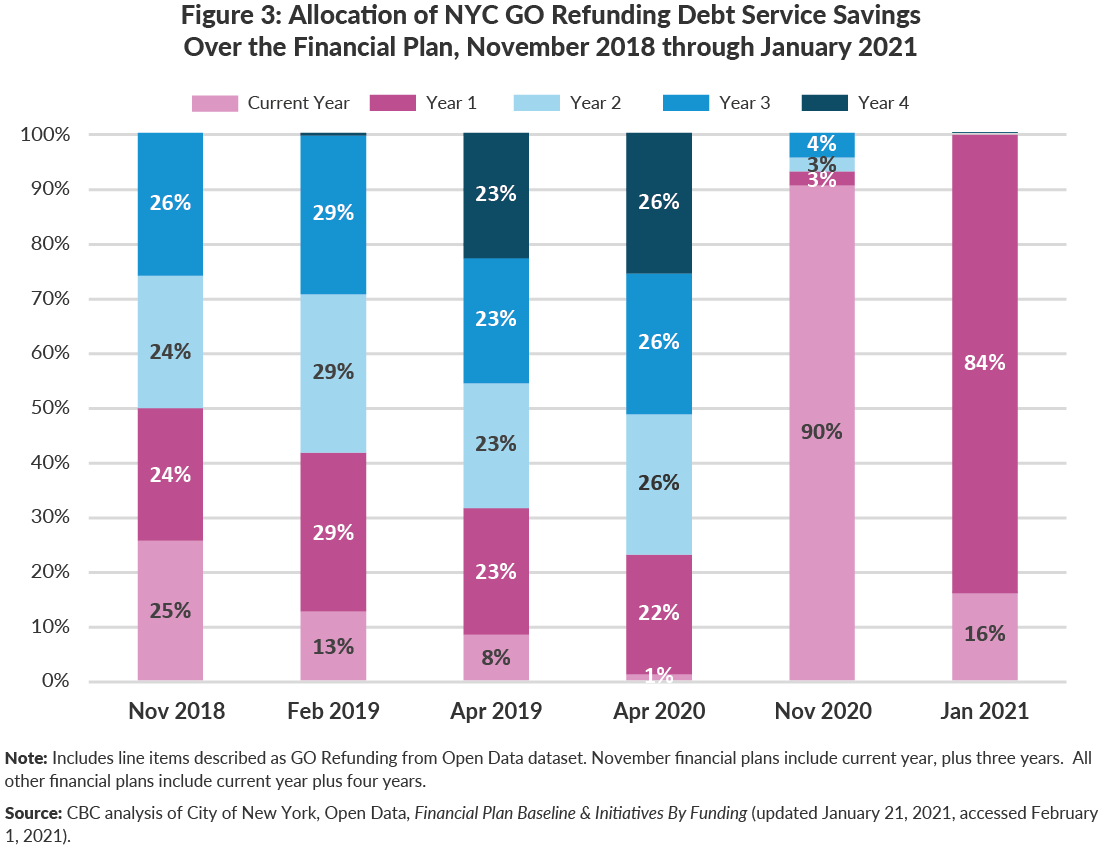

The City’s management of long-term debt, including lower interest rates on variable rate debt, savings from refunding General Obligation (GO) debt, and lower than previously assumed levels of new borrowing at lower interest rates, provided net savings of $541 million. For the two GO refunding offerings thus far in fiscal year 2021, the Administration opted to structure the deals to maximize savings in the first two years, which is a departure from the four preceding refunding offerings that spread out the savings more evenly.11 (See Figure 3). From November 2018 to April 2020, between 23 percent and 49 percent of the savings accrued to the first two years, while in the August 2020 and December 2020 refunding offerings, 93 percent and 100 percent of the savings accrued to the first two years.

Pensions

The Actuary for the City of New York has proposed a package of changes to the actuarial assumptions and methods for the City’s five pension funds.12 The package would reduce the City’s contributions in the first three years and increase them thereafter.13 Over five years, the total contributions are reduced by $17 million; however, this is the result of the reduction in contributions in fiscal years 2021 to 2023 ($430 million, $304 million, and $69 million, respectively) being offset by an increase of $350 million in fiscal year 2024 and $436 million in fiscal year 2025. (See Figure 1). Neither the Actuary nor the Office of Management and Budget provided estimates of the fiscal impact outside the financial plan years.

The proposed savings are based on the following changes to actuarial assumptions and methods:

- Lowering the assumed rate of inflation from 2.5 percent to 2.3 percent over four years, which affects three other assumptions: the actuarial interest rate, the general wage increase assumption, and the cost-of-living assumption. Lowering the actuarial interest rate to 6.8 percent over four years, from the current 7.0 percent would be prudent and bring the City’s pension funds in line with New York State’s funds. This change will increase the City liability and reduce the funding ratio because investment returns will be assumed to be lower;

- Restarting the actuarial value of assets, last done in fiscal year 2012, to reflect actual earnings through June 30, 2019. This restart speeds up recognition of better than projected investment returns in recent years; and

- Changes that adjust mortality tables, assumptions about member loans, and requiring the City to make the full annual employer contribution for the NYC Off-Track Betting Corporation.

Downside Risks Could Make Matters Worse

Four downside risks could negatively affect the City’s financial picture—three on the revenue side and one on the expense side.

If the economic recovery does not continue at the pace assumed in the financial plan, the tax revenue forecast could be overly optimistic. Currently, the City forecasts an 8.1 percent increase in non-property tax revenue in fiscal year 2022, followed by growth of 6.0 percent in fiscal year 2023. Additionally, property tax assessment challenges and delinquency could further depress revenue, though the City’s budget includes estimates for those components.14 Also, the economic recovery depends on the trajectory of private sector employment growth, the reduction of pandemic driven restrictions, and tourism returning to pre-pandemic levels over the financial plan.

In addition to a risk that fewer commuters will come into the Central Business District daily and generate economic activity, some partial or full remote work arrangements may become permanent. That, plus the proposals under consideration in the State Legislature to increase taxes on higher earners, could increase the risk of migration out of New York City or New York State, possibly dampening personal income tax and unincorporated business tax revenues.

While the State’s short-term revenue picture is rosier today, with higher than forecast tax revenues and prospects of significant federal aid exceeding $12 billion, the State’s fiscal stress rests partly on problems that preceded the recession.15 The State Executive Budget currently proposes a substantial drop in state education aid beginning in state fiscal year 2023, which would reduce the City’s funding.

While revenues could be lower, spending could be higher. Collective bargaining agreements with the City’s unions are beginning to expire, while a few contracts from the prior round remain unsettled.16 Mayor de Blasio eliminated funding for one percent raises in the first two years of the next round, so the Mayor that negotiates these contracts must secure agreement to no raises in the first two years, secure concessions to pay for raises, find additional revenues to pay for any collective bargaining increases, or the budget gaps will be increased.

Wise Use of Federal Relief Can Help in the Short and Long Run

The City is estimated to receive about $5.6 billion in direct federal aid from the American Rescue Plan Act of 2021, in addition to about $1.15 billion in additional Federal Emergency Management Agency (FEMA) reimbursement.17 This substantial funding is more than enough to wipe out the fiscal year 2023 projected $5.3 billion gap, but it will not fill the City’s gaps over the long-term. Therefore, it is essential that this Administration make prudent use of these one-time resources to provide the COVID-19 related services New Yorkers need and ensure a stable fiscal future. Federal funding should be used to:

- Support COVID-19 response expenditures not covered by FEMA;

- Fund additional costs and supports necessitated by the pandemic, such as expenditures related to school re-opening or test and trace efforts;

- Temporarily backfill shortfalls in tax revenues due to the pandemic, appropriately with a post-federal support fiscal stability plan; and

- Support residents and businesses negatively affected by the pandemic and recession, to the extent resources are available and only if needed on top of American Rescue Plan investments.

But, as a one-time revenue infusion, federal funds should not be used to support new programs or hiring that requires on-going funding. If federal aid is sufficient and flexible, the City should spread these funds over multiple years to support a glide path toward stability as the economy and tax revenues recover and the City increases the efficiency of its operations.

Federal aid does not exempt the City from implementing the hard choices needed during a time of fiscal stress: when balancing revenues and expenditures, the City should minimize negative impacts, especially for those in need; maintain the City’s competitiveness; and not burden future generations.18 The City has opportunities to implement recurring budget savings, which would not only improve the financial picture today, but for years to come. Successfully negotiating work rule changes with the City’s municipal unions and rationalizing employee benefits could yield substantial recurring savings exceeding $1 billion per year.19 The eighteen labor savings ideas put forth by CBC also include eliminating the Absent Teacher Reserve, consolidating union welfare funds, modernizing Department of Sanitation productivity differentials, and implementing employee contributions to health insurance premiums. Federal aid can be used to temporarily fill budget gaps while these long-lasting changes are negotiated and implemented.

Conclusion

The city’s early recovery has been slowed by the most recent wave of infections. With more people being vaccinated and warmer weather returning, there is hope that the recovery accelerates in the near future. This economic recovery likely will be bolstered by federal stimulus provided to residents and businesses in the city.

Nonetheless, the City faces long-term fiscal challenges and risks that were not adequately addressed by a Preliminary Financial Plan that relied on actions that balanced the budget today with insufficient regard for tomorrow. With the substantial infusion of American Recovery Plan funds—over $5 billion—the City has the opportunity to embark on the path to stability. This should not squandered by unwise use of this aid and avoidance of the necessary hard choices. The Executive Budget for Fiscal Year 2022 and ensuing negotiations between the Council and Mayor should prioritize judicious use of the new resources over two to three years to support a long-term plan for fiscal stability and effective government.

Footnotes

- On a common rate and base, since fiscal year 1999, property tax revenue has not experienced a year-over-year decline. Between fiscal years 1999 and 2019, growth, on a common rate and base, averaged 6.17 percent per year. City of New York, Office of Management and Budget, email communications to Citizens Budget Commission staff (November 30, 2018, December 4, 2018, and January 10, 2019).

- Prior CBC work details actions taken to balance the budget for fiscal year 2020 and adopt a balanced budget for fiscal year 2021. See: Ana Champeny, “NYC FY2021 Adopted Budget: Short-Term Balance, Long-Term Challenge,” Citizens Budget Commission Blog (July 21, 2020), https://cbcny.org/research/nyc-fy2021-adopted-budget.

- City of New York, Office of Management and Budget, NYC Employment Data (SA) - December 2020 (January 22, 2021).

- These are the market value reductions for Class 4 and Class 2, respectively.

- This figure reflects the fiscal year 2021 budget savings of $710 million. Total deferrals to date are $776 million, modest additional savings were realized in fiscal year 2021 due to furloughs of managerial and non-represented employees. Budget savings from deferrals are lower than the total amount payments deferred because some of the retroactive pay increases for retirees were booked as expenditures at the time of the collective bargaining agreement, despite the payment not needing to be made until now.

- The $1.3 billion gap in fiscal year 2022 assumes that the surplus roll from fiscal year 2021 to fiscal year 2022 is reduced by $290 million to cover the fiscal year 2021 labor savings, thereby widening the fiscal year 2022 shortfall by the same amount.

- Debt service savings are typically included in the CSP total. The January 2021 savings were $215.3 million in fiscal year 2021, $326 million in fiscal year 2022, $4 million in fiscal year 2024, and $34 million in fiscal year 2025; debt service costs increased by $14 million in fiscal year 2023.

- The three agencies are the Department of Social Services, the Administration for Children’s Services, and the Department of Mental Health and Hygiene.

- The hiring freeze exempts uniformed titles, teachers, health and safety titles, and revenue-generating titles. Testimony of Jacques Jiha, Director, City of New York, Mayor’s Office of Management and Budget, before the City Council Committee on Finance, Committee on Contracts, and Subcommittee on the Capital Budget, New York City Council Budget and Oversight Hearings on The Preliminary Budget for Fiscal Year 2022, The Preliminary Capital Commitment Plan for Fiscal Years 2021-2025 and The Fiscal 2021 Preliminary Mayor’s Management Report (March 2, 2021), https://legistar.council.nyc.gov/LegislationDetail.aspx?ID=4806557&GUID=D26FF644-7EF0-4D34-8CED-CA49F46F8722&Options=&Search=.

- City of New York, Mayor’s Office of Management and Budget, Preliminary Budget: Fiscal Year 2022: Citywide Savings Program (January 14, 2021), https://www1.nyc.gov/assets/omb/downloads/pdf/csp1-21.pdf.

- The fiscal year 2021 GO bonds are: 2021AB bonds of $1.4 billion, and 2021DE bonds of $1.4 billion. See: City of New York, Office of Management and Budget, January 2021 Financial Plan Detail (January 14, 2021), https://www1.nyc.gov/assets/omb/downloads/pdf/tech1-21.pdf.

- This is not unusual. The Actuary routinely presents these packages of changes following biennial audits. However, two notable difference this time around are that 1) the package is being proposed ahead of the audit due out later this calendar year, and 2) the City is reflecting the fiscal impact in the financial plan prior to securing the support of the pension boards and the necessary state legislation.

- City of New York, Office of the Actuary, Fiscal Analysis for Proposed Changes to Actuarial Assumptions and Methods Used to Determine FY2021 Through FY2021 Employer Pension Contributions (January 4, 2021).

- The property tax revenue forecast is the levy less the property tax reserve, which includes components for delinquent payments, reductions via the Tax Commission, prior year refunds, and abatements.

- For a discussion of the State’s fiscal condition and Governor Andrew Cuomo’s Executive Budget for Fiscal Year 2022, see: Patrick Orecki, Balancing Act: Alternatives that Balance the NYS Budget without Raising Income Taxes (Citizens Budget Commission, February 10, 2021), https://cbcny.org/research/balancing-act.

- The Police Benevolent Association opted for binding arbitration and hearings have been delayed due to the pandemic; the Uniformed Firefighters Association has delayed settling in hopes of the PBA receiving a better settlement. Both contracts expired on July 31, 2017. The City budget only includes funding to provide pattern wages to these two unions representing around 33,000 employees. The collective bargaining agreement with the Local 2507, the union representing emergency medical technicians and paramedics, has also not been settled due to requests for pay parity with firefighters. As to collective bargaining agreements due to expire soon, the largest is with the District Council 37, expiring May 25, 2021.

- FEMA had been reimbursing the City 75 percent of eligible COVID-19 related costs; President Biden has increased the percentage to 100, which means the City is due $1.15 billion for COVID-19 related expenditures. See: Jonathan Rosenberg, FEMA Increase to Covid Reimbursement Means Over $1 Billion More for the City (Independent Budget Office, February 2020), https://ibo.nyc.ny.us/iboreports/FEMA-increase-to-covid-reimbursement-means-over-1-billion-more-for-the-city-fopb-1-feb2021.pdf.

- Charles Brecher, A Framework for Hard Choices: Choosing Among Options to Address New York’s State and Local Fiscal Stress (Citizens Budget Commission, May 22, 2020), https://cbcny.org/research/framework-hard-choices; and Ana Champeny, Hard Choices That Can Balance New York City’s Budget (Citizens Budget Commission, June 10, 2020, https://cbcny.org/research/hard-choices-can-balance-new-york-citys-budget.

- Ana Champeny and Maria Doulis, How to Make $1 Billion in Labor Savings Real & Recurring (Citizens Budget Commission, September 2, 2020), https://cbcny.org/research/how-make-1-billion-labor-savings-real-recurring.