11 Billion Reasons to Rethink

New York's Increasing Economic Development Spending

HIGHLIGHTS

- State and local governments in New York spend a lot on economic development: nearly $11 billion annually between tax breaks and direct spending.

- After holding steady in recent years, economic development spending has started to increase again—and likely will increase more in the coming years, potentially exceeding $13 billion in 2025.

- Spending continues to increase even though State and local governments don't know if this spending is effective: poicymakers should conduct through, data-driven evaluations of effectiveness of incentives and grant programs and use the findings to eliminate or reform programs that are found ineffective.

New York State and its localities’ spending on economic development programs has long exceeded spending in nearly every other state. Despite improved disclosure about individual projects, State and local economic development spending continues to increase without sufficient evidence that these programs cost-effectively create jobs or are more beneficial than alternative uses of the funds.

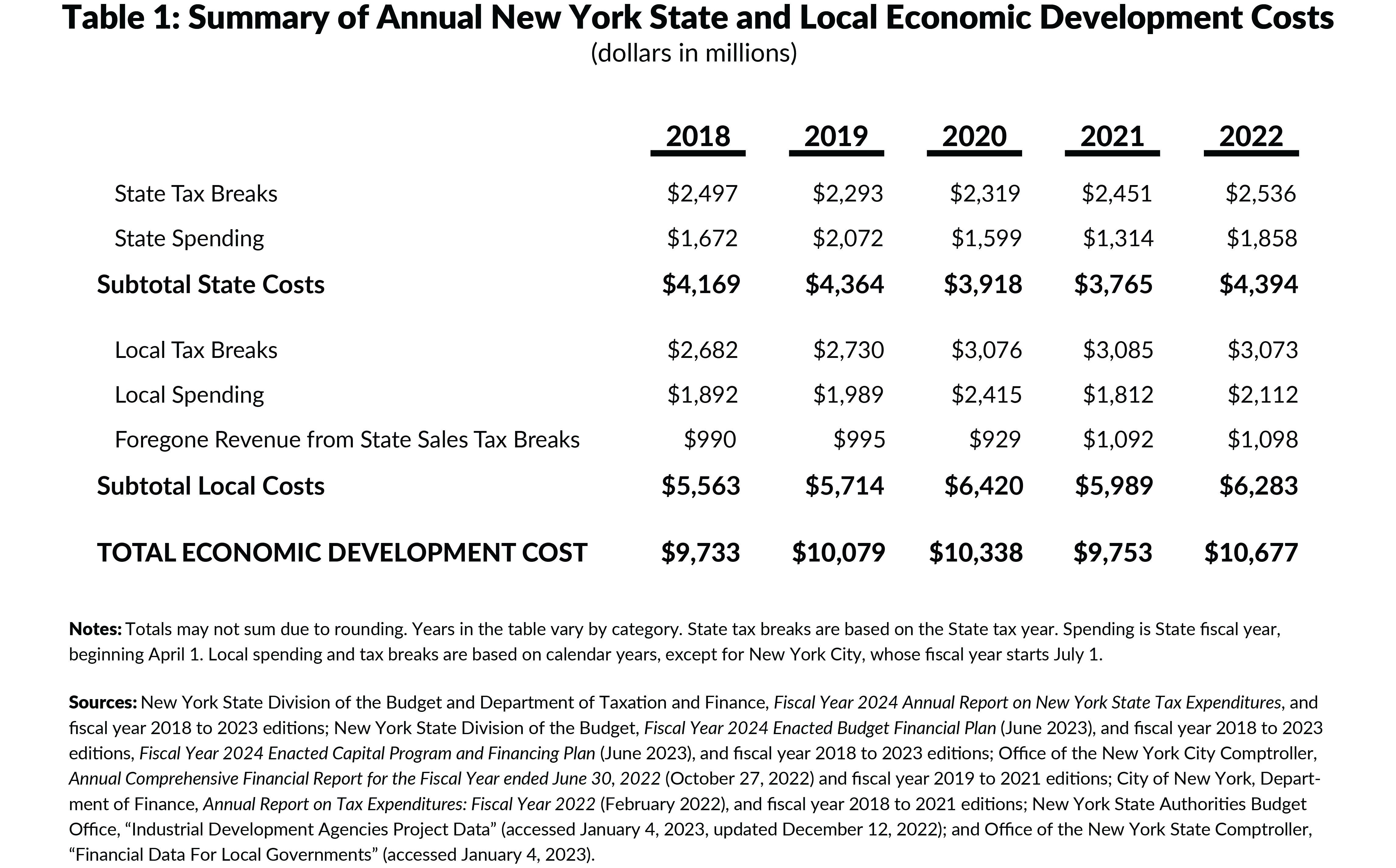

This update to the Citizens Budget Commission’s (CBC) previous accounting of economic development spending finds that State and local economic development spending in New York totaled $10.7 billion in 2022, the highest level since CBC began tracking this spending.

Specifically, CBC’s analysis of economic development spending in 2022 finds that:

- State economic development spending totaled nearly $4.4 billion, including $2.5 billion in foregone revenue from tax expenditures and $1.9 billion in direct spending; and

- Local and county government spending cost $6.3 billion, including $3.1 billion in tax breaks, $2.1 billion in direct spending, and an additional $1.1 billion in foregone local sales tax revenue resulting from State sales tax exemption programs.

Economic development spending could reach $13 billion annually by 2025 based on spending increases and expanded incentives approved by the State in recent years:

- The cost of existing incentive programs is projected to increase by $500 million in 2023, a 22 percent increase from fiscal year 2022, and could increase by another $1 billion annually starting in 2024 as three new and expanded programs take effect:

- The expansion of the film tax credit increased the annual cap from $420 million to $700 million per year;

- The extension of the theatrical production increases the lifetime cap of the tax break by another $100 million to $300 million;

- Green CHIPS will increase expenditures as much as $500 million per year if fully utilized; and

- Direct State capital spending on economic development is projected to double to nearly $4 billion annually by 2025.

New York State and its localities should not spend such massive resources absent evidence they have created or are substantially likely to create jobs that otherwise would not exist. The State faces a $9.1 billion budget gap next year and a $13.4 billion gap in fiscal year 2027. Squandering precious resources will put the State’s economy and finances at risk. It is critical to use data-driven analytics to determine whether to create, continue, expand, better target, or eliminate economic development programs and incentives.

Specifically, CBC recommends the State and its localities:

- Rigorously evaluate existing incentives and programs to determine their effectiveness;

- Narrow, shrink, or eliminate programs that are not proven effective;

- Adopt performance-based incentives whenever possible;

- Create a unified economic development budget; and

- Increase oversight powers of the State Comptroller and Authorities Budget Office.

STATE AND LOCAL ECONOMIC DEVELOPMENT COST $10.7 BILLION IN 2022

State, county, and local governments in New York spent $10.7 billion on economic development in 2022. This total includes the cost of both foregone revenue via tax breaks and direct spending, which includes both capital outlays and operating expenses. Costs are split between the State and localities, with a majority borne by counties and local governments. (See Table 1.)

CATEGORIES OF ECONOMIC DEVELOPMENT INCLUDED IN THIS REPORT

There is no standard definition of economic development spending in the academic literature or State law. As a result, economic development suffers from definitional and categorical vagueness: it can encompass workforce development and training programs, place-based revitalization strategies, direct business assistance and tax breaks, arts and culture funding, sports facilities, and infrastructure projects.

For this report, CBC includes tax expenditures, direct spending, and capital borrowing that is intended to spur economic growth, to support the well-being of specific economic sectors, or to promote job creation. Spending is counted if programs or projects are funded through an economic development agency or explicitly labeled as economic development, except for cases in which routine operating expenses for non-economic development activities were shifted to an off-budget economic development entity. (Examples of excluded spending include funding for the New York State Thruway, hospitals, and counterterrorism.) Tax breaks are counted if their intent is to grow the economy or to attract economic activity to specific areas. For example, business attraction or retention incentives are included, but incentives for residential development or tax breaks on certain consumer goods like clothing are not.

State Economic Development Spending

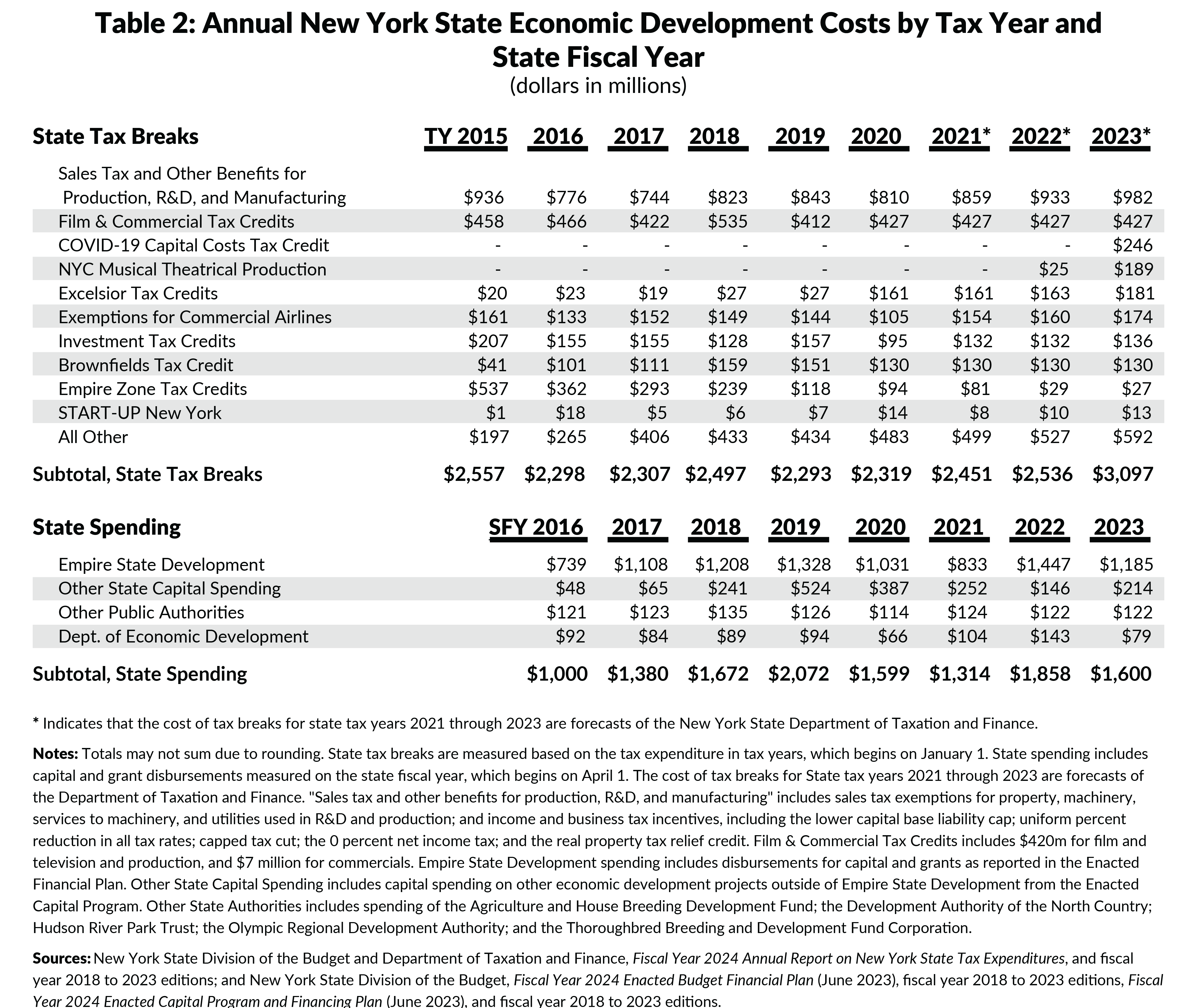

Tax breaks make up two-thirds of State economic development spending. Another third of the State cost of economic development is direct State spending. (See Table 2.)

State Tax Breaks

After holding steady in recent years, the cost of tax breaks is projected to increase in tax year 2023 and beyond. According to the New York State Department of Taxation and Finance’s estimates, the cost of economic development tax breaks varied between $2.3 billion and $2.5 billion between tax years 2018 and 2022 before increasing to $3.1 billion in tax year 2023. The cost could increase even more in future years based on recently adopted laws.

The estimated cost of tax breaks remained relatively steady through 2022, with the two largest programs comprising over 50 percent of State economic development tax breaks:

- Tax benefits for manufacturing and production companies cost $933 million in 2022. These tax breaks reduce energy and utility costs used in manufacturing and research and development; exempt the purchase, maintenance, and repair of machinery and equipment used in production from the state sales and use tax; and reduce the business income tax rate for qualified manufacturing firms.

- The film and television production and post-production tax credits are now the second largest tax break, even before accounting for the credit’s expansion in the Fiscal Year 2024 Enacted Budget. Prior to the recent expansion, the film tax credit offered a fully refundable 25 percent credit on production and post-production costs, with the total amount of credits capped at $420 million per year. Demand for the credit from film productions regularly exceeds the cap: the State has issued credits exceeding the $420 million cap in the last four years. Once the cap is reached, the State allows awardees to claim credits in future years.

As the Empire Zone program winds down, spending on its replacement, the Excelsior program, has ramped up but stayed at lower absolute levels:

- The expenditure for the Empire Zone tax credit program, once one of the country’s costliest economic development programs, continues to steadily decline as the program winds down.1 The cost has fallen from its peak of $537 million in 2015 to $29 million in 2022. The program has long been closed to new applicants.

- The tax expenditure for the Excelsior program, which replaced the Empire Zone program, is steadily increasing, reaching $163 million in 2022, but so far remains at a lower level than its predecessor. Excelsior is a discretionary program awarded by the Empire State Development Corporation (ESD) that provides tax credits to businesses who relocate to or expand in New York and meet specific thresholds for job creation and investment. The amount of new Excelsior tax credits that can be awarded each year is capped under State law; Taxation and Finance’s estimate includes the cumulative cost of previously awarded credits in a given tax year.

The cost of tax breaks is likely to increase in 2023 and beyond. Taxation and Finance projects that foregone revenue from State tax breaks will reach $3.1 billion in State tax year 2023. If accurate, this would be a 22 percent increase from the previous year and the highest level since tax year 2015, when the now-defunct Empire Zone program began to wind down. (Note that Taxation and Finance estimates could be adjusted or amended in future years to reflect actual tax collections and credit applications.)

Two incentives created as part of the State’s COVID-19 response rank among the State’s costliest in State tax year 2023 and drive much of this increase:

- The COVID-19 Capital Costs Tax Credit, projected to total $246 million in tax year 2023, provides tax benefits to reimburse small businesses for a variety of qualified expenses incurred during the pandemic. The lifetime cost of the program is capped at $250 million.

- The New York City Musical and Theatrical Production Tax Credit, which is expected to cost $189 million in tax year 2023, was intended to help stabilize New York’s theater industry during its reopening period.

Three additional actions could increase the cost of economic development incentives by another $1 billion per year starting in tax year 2024:

- The Fiscal Year 2024 Enacted Budget extended the film tax credit and increased the annual cap from $420 million to $700 million, while also making it more valuable to individual productions.2

- The 2024 budget also extended the Theatrical Production credit through 2025 and increased the cap from $200 million to $300 million, despite the continued recovery of tourism and Broadway attendance.

- New York’s Green CHIPS program, enacted by the State Legislature in June 2022, will award tax breaks to semiconductor manufacturers that open facilities in New York and avail themselves of the incentive program. Green CHIPS is a performance-based incentive that offers tax breaks for job creation, capital investment, and research and development spending to qualified semiconductor manufacturing firms. The annual value of Green CHIPS credits is capped at $500 million per year through tax year 2041. The recently announced Micron project stands to receive a significant share of that cap. Micron has proposed to build four semiconductor fabs at a total cost of $100 billion; at full build out, it anticipates employing 9,000 workers. If the project starts on schedule in 2026 and meets its job creation and investment targets, Micron will receive annual Excelsior Green CHIPS tax breaks worth $122 million in 2026, increasing to a maximum of $378 million in 2038 before tapering off. Micron will also receive property tax discounts worth another $3.5 million annually in its first year, escalating 2 percent annually, and construction sales and use tax exemptions that could total $1.2 billion over the life of the project.3

Direct State Spending

Direct spending constitutes the remaining one-third of State economic development spending. This includes one-time discretionary grants, capital spending, and the cost of agency operations. Spending peaked in State fiscal year 2019. The decline in fiscal years 2020 to 2022 is attributable primarily to the completion of large projects like Moynihan Station and the renovation of Javits Center, and the winding down of major Cuomo Administration initiatives like the Buffalo Billion.

This spending also includes discretionary funding provided by the State to individual companies, non-profits, and local governments. These discretionary grants include ESD grants recommended by the Regional Economic Development Councils, which typically total $75 million to $90 million annually, and the New York Works economic development fund, which provided $230 million in discretionary grants in 2023 for infrastructure and business expansion. However, this represents only a small portion of REDC spending; most of the funds reviewed by REDCs are not included in this analysis since they do not fit CBC’s definition of economic development.

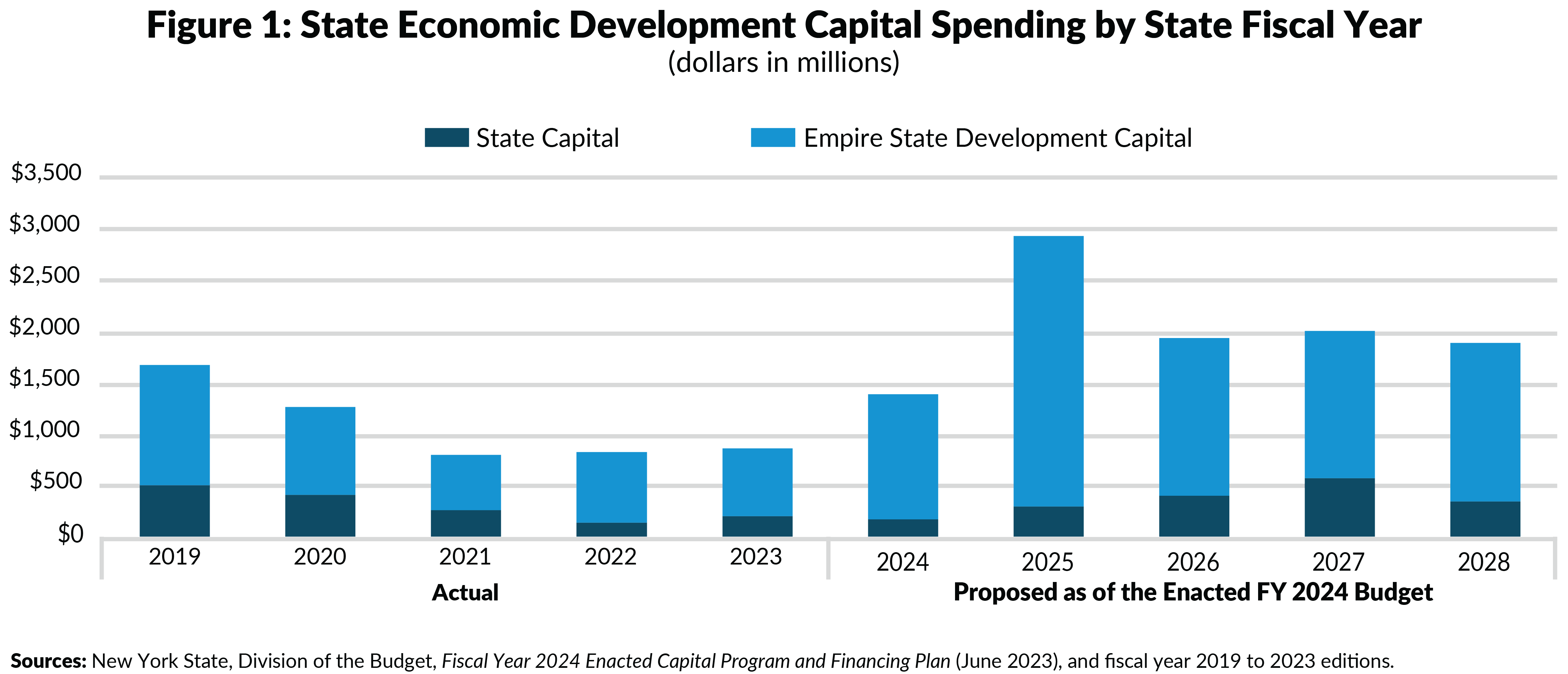

The State’s Fiscal Year 2024 Enacted Budget Capital Program and Financing Plan projects that economic development capital spending will increase from $928 million in fiscal year 2023 to $3 billion by fiscal year 2025 and remain at $2 billion annually thereafter. (See Figure 1.)

This projected growth is driven both by new initiatives and the growth of existing programs. The five-year financial plan includes funding for:

- $1.5 billion for the ConnectALL broadband program (State funding of $376 million and federal funding of $1.1 billion);

- $1.3 billion for the renovation of Penn Station as part of the Empire Station Complex project;

- $600 million for a new Buffalo Bills stadium;

- $500 million for the offshore wind industry;

- $454 million for the renovation of Belmont Raceway; and

- $350 million for a newly created Long Island Investment Fund.

In addition to these new initiatives, the State plans to increase funding for economic development through its grantmaking programs, including awarding $1.6 billion to businesses through New York Works Investment Fund from fiscal year 2024 through fiscal year 2028 and another $1.3 billion in funding through the Regional Economic Development Councils over the same period.

EXPIRING FEDERAL COVID-RELATED AID COULD DRIVE INCREASE IN SOME STATE SPENDING

The expiration of COVID-related aid also could drive State economic development spending higher in the future. Federal aid likely offset some economic development spending that the State might alternatively have funded directly. New York State received $13.5 billion from the State and Local Fiscal Recovery Funds under the federal American Rescue Plan Act, while localities received additional direct allocations. While this revenue was intended primarily to replace revenue lost due to effects of the pandemic, some of it supported recovery projects that in the past may have been considered economic development spending. The end of this aid could create pressure to maintain current levels of spending—a fiscal cliff.

Local Economic Development Tax Expenditures

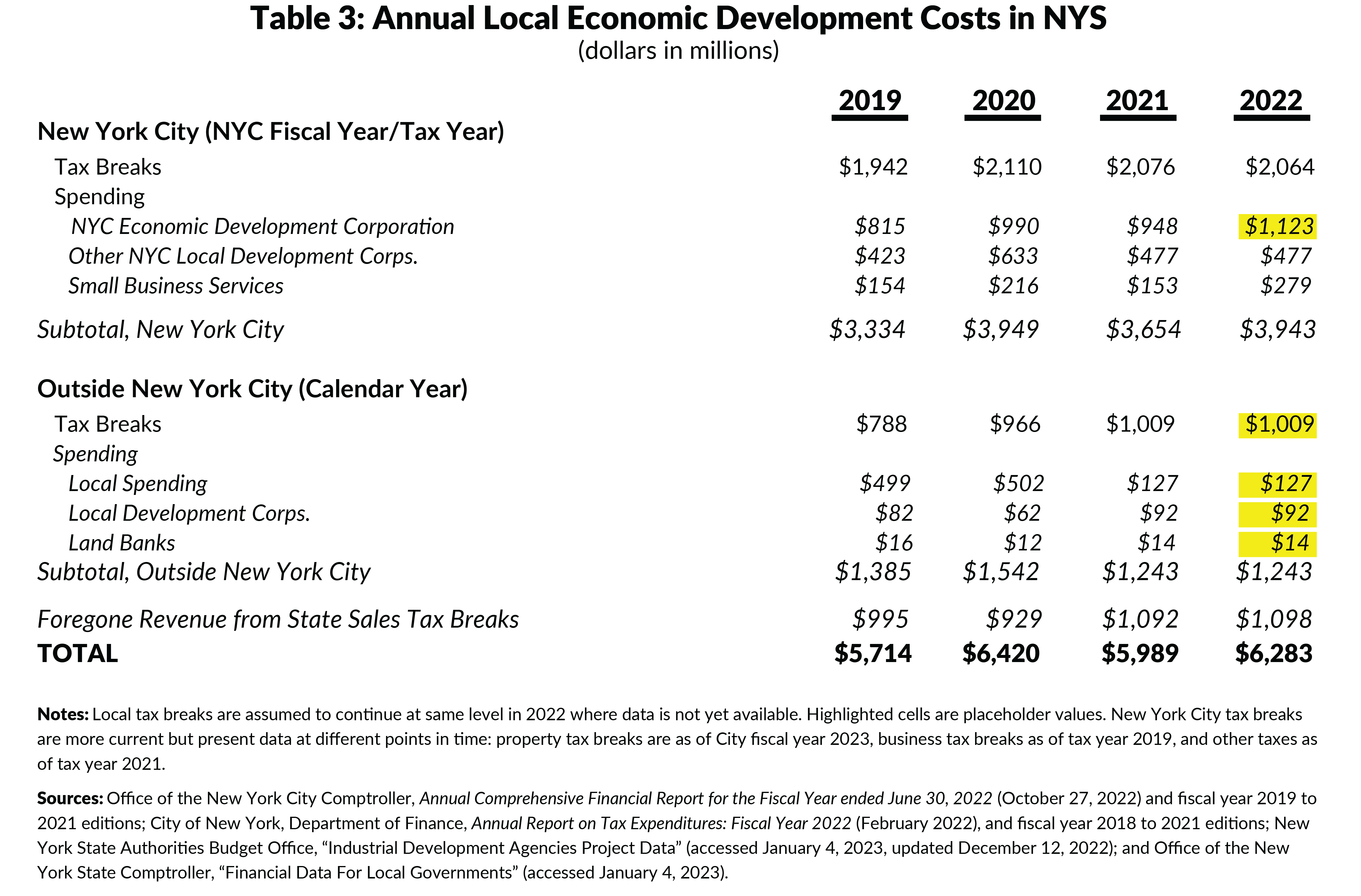

Local and county governments spend another $6.3 billion on economic development. (See Table 3.) Most local economic development activity flows through local Industrial Development Agencies (IDAs) and other local development corporations (LDCs). IDAs and LDCs are non-profit entities wholly controlled by local or county governments but independent of many of the procurement and financing restrictions that apply to public entities.4

New York City

New York City represents the vast majority of both local tax breaks and spending. New York City accounts for two-thirds of the local and county tax expenditures and roughly 90 percent of local spending.

New York City tax breaks reported in the fiscal year 2023 tax expenditure report totaled an estimated $2.1 billion, including $841 million for the now expired Industrial and Commercial Incentive Program and its successor the Industrial and Commercial Abatement Program; $613 million for insurance corporation non-taxation; $576 million in property tax discounts and exemptions granted by the NYC IDA or the NYC Economic Development Corporation (EDC); and $81 million for a variety of smaller programs.5

Of the $1.8 billion in local economic development spending by New York City in City fiscal year 2022, the Economic Development Corporation (EDC) accounted for about 60 percent, including both programs funded through its operating budget and the value of capital projects managed by EDC on behalf of other agencies. Another $477 million was spent by other local development corporations in the city, including the Hudson Yards Infrastructure Corporation and the Brooklyn Navy Yard Development Corporation. On-budget operating spending was concentrated primarily in the Department of Small Business Services, which spent $279 million in 2022, net of pass-through payments to EDC.

Outside New York City

IDAs outside New York City granted another $1.0 billion in tax breaks, including discounts on sales, real property, and mortgage recording taxes, for companies and development projects in calendar year 2021, the last year for which data are available.

Local and county governments outside New York City collectively spent $234 million in calendar year 2021, including costs incurred by municipalities, counties, local development corporations, and land banks. (Spending for 2022 is not yet available but assumed to continue at the 2021 level.)

Finally, when the State creates a sales tax break for economic development, those tax breaks also result in foregone revenue for county and local governments. (The base State sales tax rate is 4 percent, with an additional 0.375 percent imposed in the Metropolitan Commuter Transportation District. Local and county governments impose an additional 4 to 4.875 percent on top of the State’s tax.) This analysis conservatively assumes that the local tax expenditure for sales tax breaks is equal to Taxation and Finance’s estimate for the State tax expenditure. In 2022, State sales tax breaks resulted in an estimated additional $1.1 billion in foregone tax revenue by local and county governments.

CONCLUSION

Given the significant budget gaps in New York State and City and likely increases in economic development spending despite a lack of evidence of impact, State and local leaders must evaluate these programs to determine cost-effectiveness, reform or eliminate those not found to be effective, and increase transparency and accountability for results.

There has been some notable progress on transparency in recent years. Despite some shortcomings that could limit the timeliness and comprehensiveness of reporting, the recently codified “Database of Deals” creates a standard definition of a job and increases visibility into State spending and whether subsidy recipients meet job creation goals.6 State leadership has publicly released term sheets for major projects like Micron.7 And the State Department of Taxation and Finance has commissioned a study of the total cost, economic impact, and effectiveness of economic development tax incentives.8

Despite these improvements, the State continues to expand existing incentives without evidence that they are necessary or cost-effective. In some cases, State officials have extended or expanded incentives despite independent evaluations showing that the credits are ineffective.9

CBC advocates reform of State economic development policy, including a unified economic development budget; the use of performance-based incentives; thorough evaluations to determine what works and what does not; and increased oversight by the State Comptroller and Authorities Budget Office.

Transparency and evaluation are necessary first steps but on their own are insufficient to ensure that economic development policy is effective or efficient. State and local elected officials should commit to using evidence to reform or eliminate ineffective programs or spending.

Footnotes

- Elizabeth Lynam and Tammy Pels, It’s Time to End New York State’s Empire Zone Program (Citizens Budget Commission, December 2008), https://cbcny.org/sites/default/files/report_ez_12012009.pdf?fbclid=IwAR1aH; and Sean Campion, NY’s Economic Development Programs Costliest in the Nation (Citizens Budget Commission, April 7, 2017), https://cbcny.org/research/nys-economic-development-programs-costliest-nation.

- Adam Ciampaglio and Sean Campion, Shrink, Don’t Expand the New York State Film Tax Credit (Citizens Budget Commission, March 6, 2023), cbcny.org/research/shrink-dont-expand-new-york-state-film-tax-credit.

- New York State Empire State Development, Key Terms and Conditions for Development of the Micron Green Manufacturing Memory Chip Fab Campus in Clay, New York (September 22, 2022), https://esd.ny.gov/sites/default/files/Micron-Term-Sheet-Fully-Executed.pdf.

- Note that this analysis does not include on-budget local or county appropriations, some of which may constitute additional economic development activity.

- New York City tax breaks are reported annually in the Tax Expenditure Report but present data at different points in time: the 2023 report provided property tax breaks as of City fiscal year 2023, business tax breaks as of tax year 2019, and other taxes as of tax year 2021. See: City of New York, Department of Finance, Annual Report on Tax Expenditures: Fiscal Year 2023 (February 2023), https://www.nyc.gov/assets/finance/downloads/pdf/reports/reports-tax-expenditure/ter_2023_final.pdf.

- Andrew S. Rein, “Statement on Economic Development Database and Film Tax Credit in the Fiscal Year 2023 Enacted Budget” (Citizens Budget Commission, April 8, 2022), https://cbcny.org/advocacy/statement-economic-development-database-and-film-tax-credit-fiscal-year-2023-enacted.

- New York State Empire State Development, Key Terms and Conditions for Development of the Micron Green Manufacturing Memory Chip Fab Campus in Clay, New York (September 22, 2022), https://esd.ny.gov/sites/default/files/Micron-Term-Sheet-Fully-Executed.pdf.

- New York State Department of Taxation and Finance, “Request for Proposals 22-100: Economic Impact of New York State Tax Incentive Programs” (August 11, 2022), https://www.tax.ny.gov/pdf/procurement/rfp-22-100-economic-impact-study.docx.

- Adam Ciampaglio and Ana Champeny, “No Extension without Evaluation: Reject Proposed Extension of Certain NYC Economic Development Incentives Absent Appropriate Analysis,” Citizens Budget Commission Blog (February 23, 2023), https://cbcny.org/research/no-extension-without-evaluation.