Union-Administered Benefit Funds

Getting More Out Of A Billion Dollar Taxpayer Contribution

In fiscal year 2018 New York City taxpayers are projected to contribute $1.1 billion to 108 union-administered benefit funds. These funds pay for supplemental health, legal, and educational benefits or function as annuities to supplement retiree pension income for members. Many funds incur excessive administrative expenses, build unnecessary reserves, or suffer from mismanagement. In the near term, the City Comptroller’s oversight should be strengthened to address these shortcomings. In the long term, the City and labor unions should restructure how these supplemental benefits are provided. Doing so has the potential to create more than $160 million in savings for the City and improve the benefits to which members have access.

Overview of Benefit Funds

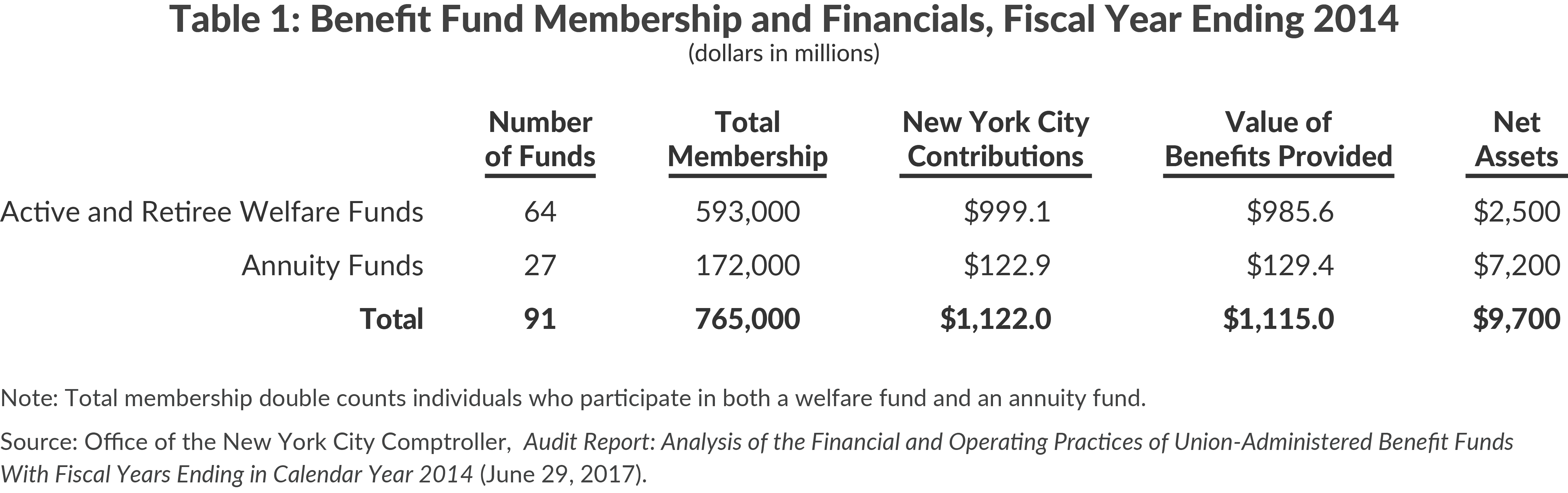

Union benefit funds are trusts established by unions representing New York City public employees to provide supplemental benefits to their members. They are funded primarily by City contributions. In fiscal year 2014 the City contributed $1.1 billion to 108 union-administered benefit funds operated by 58 separate unions, which in turn paid out more than $1 billion in benefits.

Benefit funds are operated by the unions in accordance with Trust agreements made with the City. The New York City Comptroller establishes accounting, auditing, and financial guidelines in Directive #12 of the Comptroller’s Internal Control and Accountability Directives.1 Directive #12 also requires that the funds report annual financial and operating data to the Comptroller, who produces a review of funds’ financial and operating practices based on that reporting. This analysis focuses on the 91 benefit funds included in the June 2017 review covering fund financial data for fiscal years ending in 2014.2 (See Table 1.)

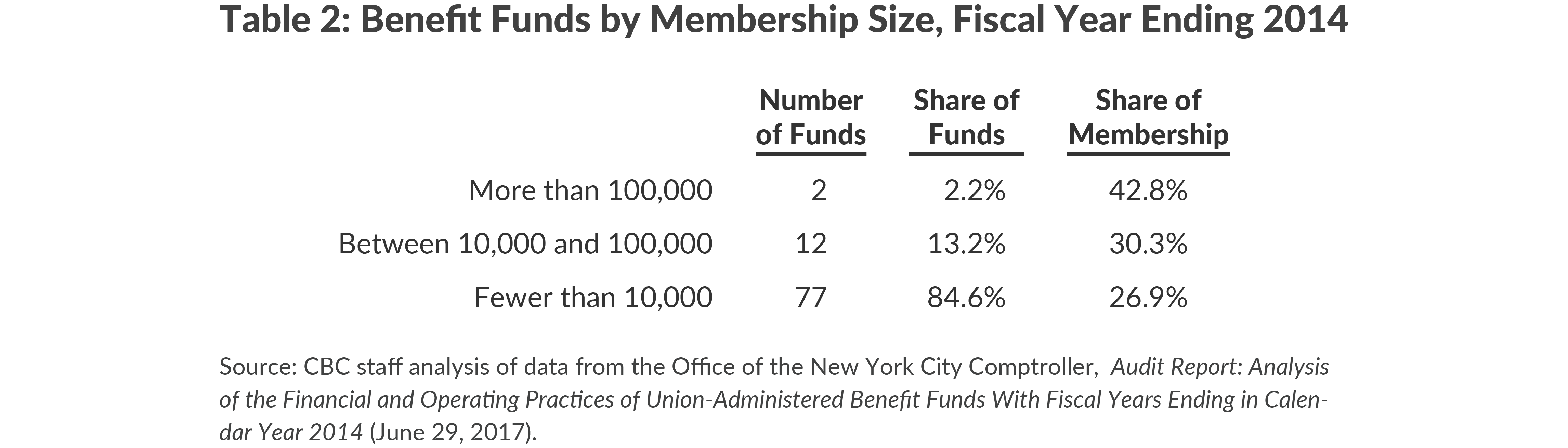

The two largest funds, those of District Council 37 (DC 37) and United Federation of Teachers (UFT), serve 42.8 percent of the total fund membership. Most funds serve few people: 85 percent of funds serve just 27 percent of total union fund members. (See Table 2.) Benefit funds fall into two distinct categories: welfare funds and annuity funds. Of the 91 benefit funds reviewed in fiscal year 2014, 64 were welfare funds and 27 were annuities.

1. Welfare Funds: Active and retired city employees receive generous health insurance benefits at a significant cost to taxpayers: in fiscal year 2018 New York City is projected to spend $6.3 billion on health insurance benefits.3 City-funded health benefit plans cover hospital and medical insurance and are administered centrally by the City for all beneficiaries. To supplement this health insurance, many unions establish welfare funds to provide dental, optical, and prescription coverage and nonhealth benefits, such as tuition reimbursement and legal services. The benefits are funded almost entirely by City contributions which are administered by union representatives.4

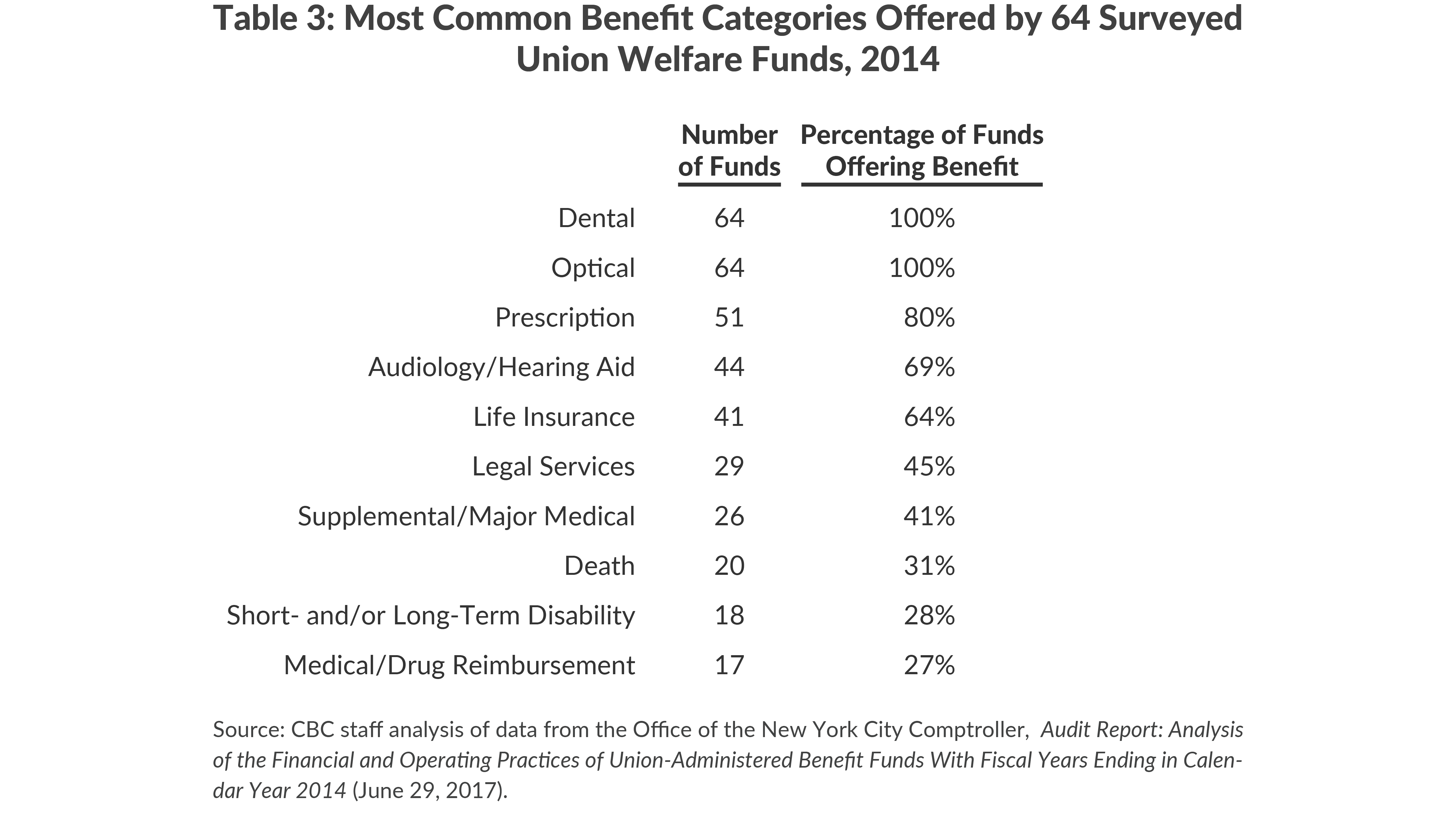

One of the advantages of having separately administered welfare funds is that each union can specifically tailor a benefits package to its membership. The Comptroller’s review of 64 welfare funds found, however, that many offer the same categories of benefits. As shown in Table 3, all surveyed funds offered dental and optical benefits, and nearly 80 percent offered prescription benefits. In a 2010 survey of three large welfare funds, the Citizens Budget Commission (CBC) found that 57 percent of benefit expenditures went toward prescriptions and 29 percent paid for dental care. Optical benefits, while ubiquitous, are relatively less costly, accounting for less than 1 percent of benefit expenditures.5

2. Annuity Funds: In fiscal year 2018, the City is projected to contribute $9.6 billion into its five defined-benefit pension funds from which retirees are paid. To supplement this pension income, 32 unions have negotiated with the City to establish separate annuities that also pay out upon retirement. The largest of these funds are District Council 37 (32,000 members), the Patrolmen’s Benevolent Association (31,000 members), and the Uniformed Firefighters Association (18,000 members). Similar to the welfare funds, these annuities are administered by union representatives and are funded by annual contributions made by the City: in fiscal year 2014 the City contributed $122.9 million to the 27 annuity funds included in the Comptroller’s report. Annuities also earn investment income; net assets totaled $7.2 billion in fiscal year 2014.

New York City Employer Contributions

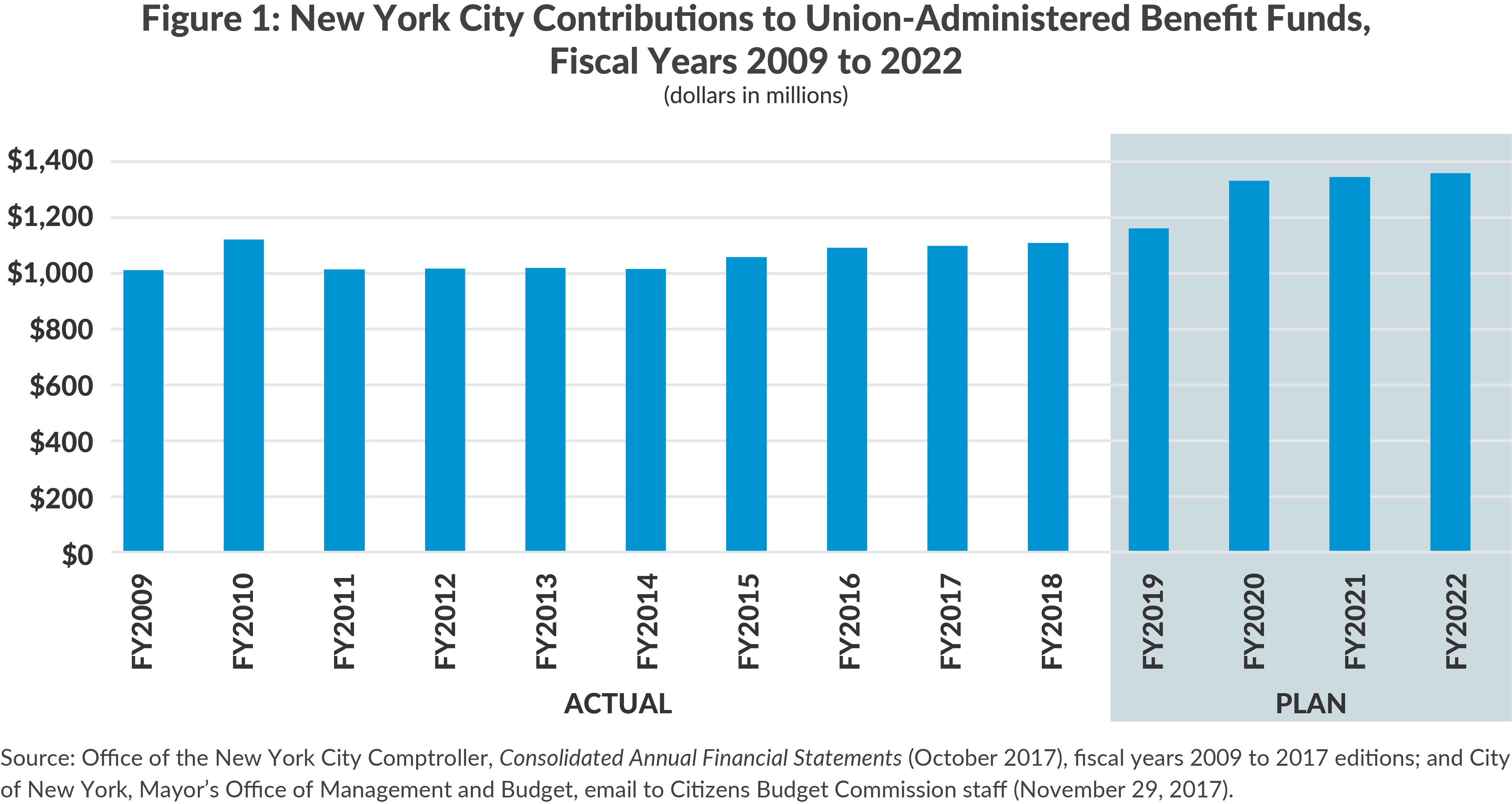

The value of City contributions to benefit funds is typically a per capita contribution agreed to in collective bargaining. In fiscal year 2016, the mean contribution for a welfare fund participant was $1,676 with contributions ranging between $830 and $2,853.6 The mean contribution for an annuity fund member is an additional $714. The value of contributions has typically increased in each round of bargaining with total contributions fluctuating based on overall fund membership. As shown in Figure 1, total contributions into the benefit funds are $1.1 billion in fiscal year 2018 and are forecasted to grow to almost $1.4 billion in fiscal year 2022.7

Benefit Funds Are Inefficient

Information on the funds’ operations is provided by the Comptroller’s office through its annual report assessing funds’ financial and operating practices and occasional audits of individual funds. The audits and annual reports reveal that many funds have problems with: (1) excessive administrative expenses, (2) unnecessary reserves, or (3) mismanagement.

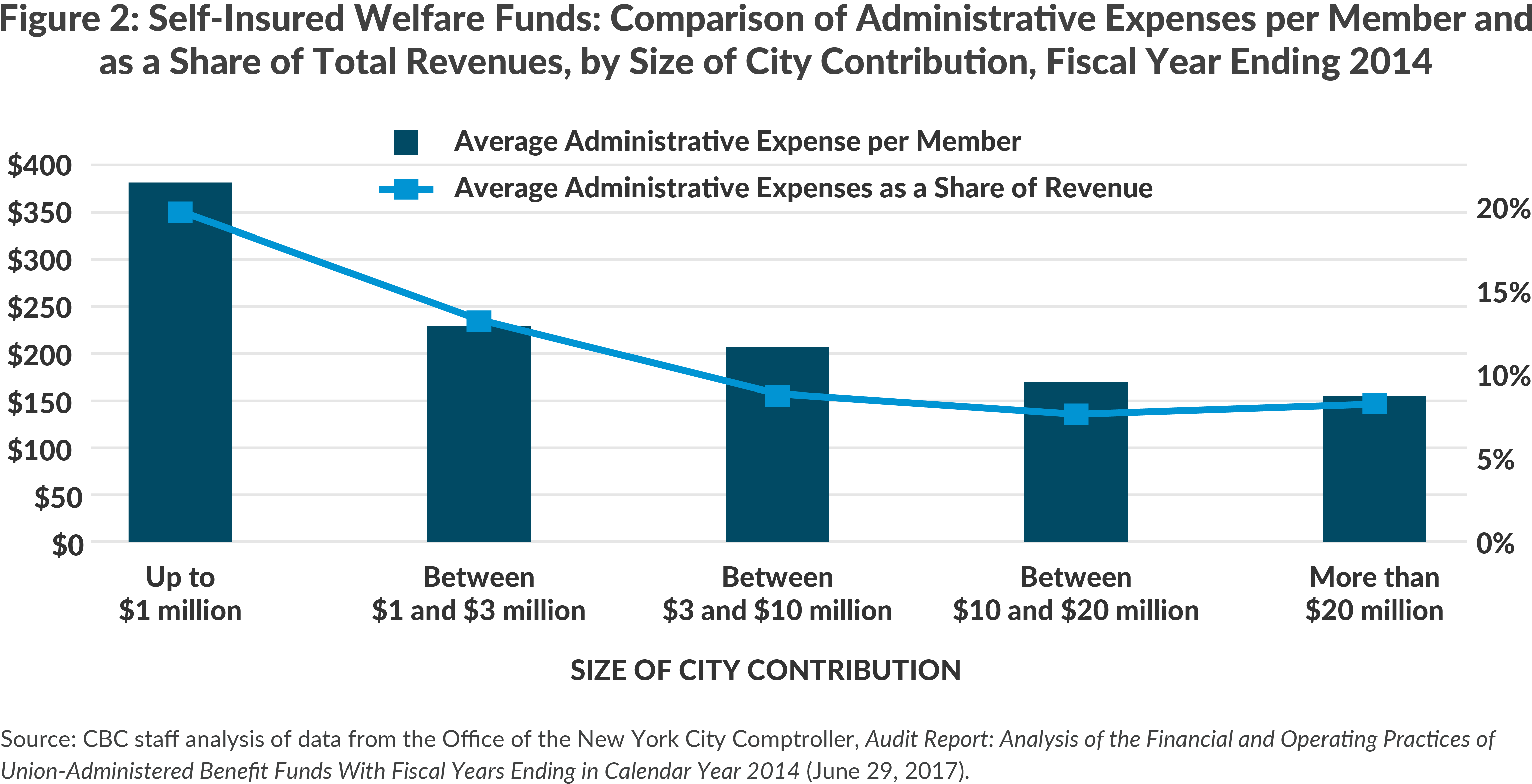

Excessive Administrative Expenses: In fiscal year 2014, the 91 benefit funds reviewed by the Comptroller spent $109.3 million on administrative expenses, or 8.9 percent of all benefit fund expenditures. Administrative burdens vary significantly and size matters: smaller funds cannot realize economies of scale and devote a larger share of their revenues to administration. Figure 2 shows that funds with smaller membership have higher administrative costs per member and a higher share of revenues going to administration.

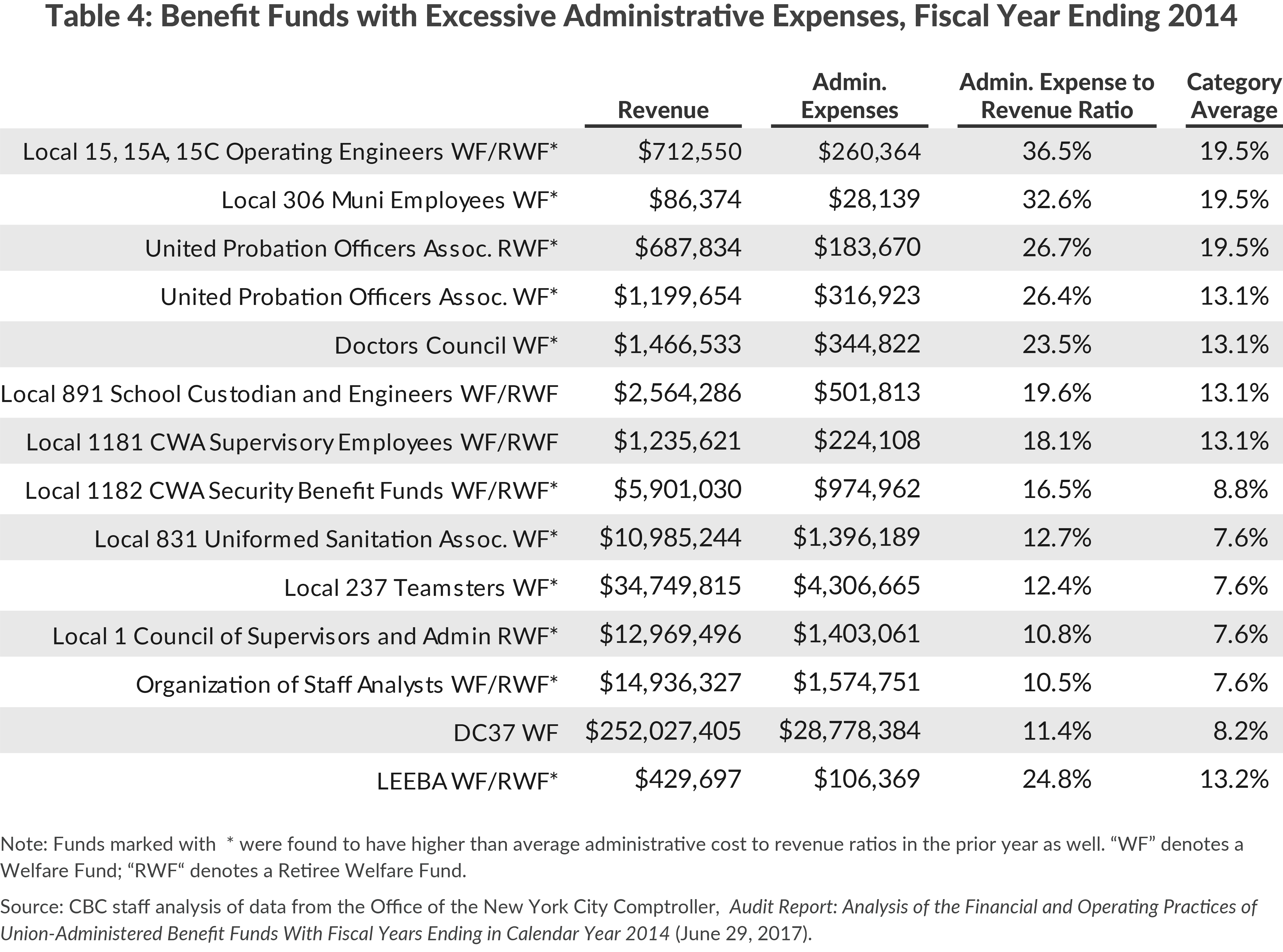

The Comptroller’s analysis compares each fund’s administrative expenses only with funds of a similar size. As shown in Table 4, the analysis found 14 funds with excessively high administrative cost to revenue ratios compared to their fund category average.8 The table shows excessive administrative expense is not a problem unique to smaller funds–DC 37’s welfare fund with $252 million in revenues makes the list. All but three of the funds highlighted were found to have higher than average administrative costs in prior years, suggesting a persistent issue.

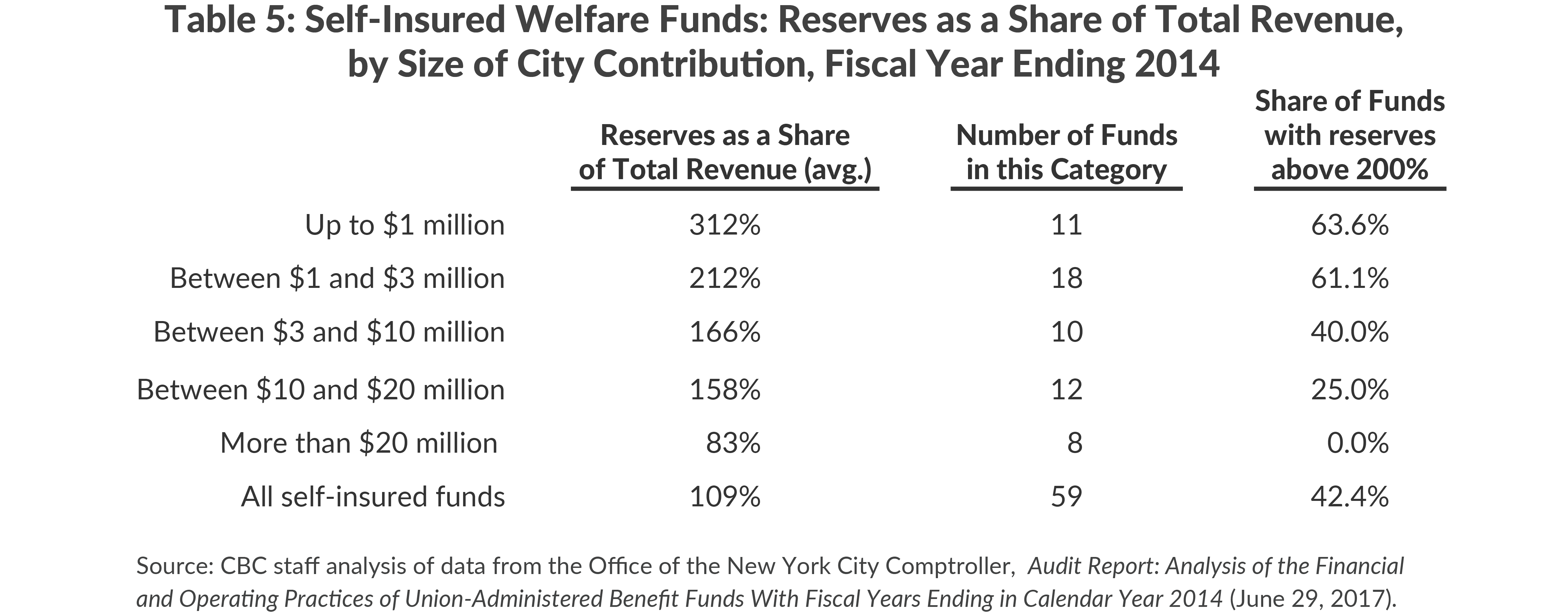

Unnecessary Reserves: Unnecessary reserves mean that the City’s contributions are going unused or a fund is not maximizing the benefits it could provide its members. Smaller funds are more likely than larger ones to maintain excess reserves. The fiscal year 2014 Comptroller’s report identified 27 welfare funds in which reserves were above what is considered to be reasonable, defined as 200 percent of annual revenues. Each of these funds was also found to have excessive reserves in the prior year. As is shown in Table 5, 63.6 percent of funds receiving less than $1 million in City contributions had unreasonably high reserves, while none of the funds receiving more than $20 million in City contributions did.

Fund Mismanagement: Numerous audits by the Comptroller cite mismanagement as an issue and identify varying degrees of management deficiencies. A 2011 audit of the Social Services Union Welfare Fund found that the fund reimbursed two dental assistants $288 dollars for sneakers.9 A 2009 audit of the Superior Officers Council Health and Welfare Fund found that it did not have documentation to support $3.1 million in benefit payments, 71 percent of its total benefit payments.10

The findings of a recent audit of the United Probation Officers Association’s Welfare Fund, published in May 2017, found: failure to properly track employee hours, provision of in interest-free loan to an employee without written agreement, prohibited stipends to trustees, failure to verify dependent eligibility, questionable benefit claims, and failure to inform members for which benefits they were eligible.11 An accompanying audit of the union’s retiree welfare fund found that no records were kept of hours worked despite spending $183,670 on employee compensation. The last time this fund was audited, in June 2009, other irregularities were found: it was determined the fund had made $140,000 in questionable or improper payments, and it produced fictitious minutes for Board of Trustees meetings.12

Short-term and long-term actions should be taken to reduce administrative costs, control reserve levels, and improve management practices.

Short Term: Improve Oversight

The Comptroller’s oversight of benefit funds should be strengthened. The annual reports focus on overall revenues and expenditures without examining details through which mismanagement is most likely to be identified. While the reports indicate which funds are outliers on certain metrics, they neither determine why nor make specific recommendations as to how funds could better comply with Directive #12 guidelines. The reports are not timely as they are often delayed by the tardy submittal of financial information from the union funds.

The Comptroller’s audits of individual funds should be more frequent and numerous. Between 2009 and 2017 there were 11 audits of 9 funds, and only $44.5 million out of $10.3 billion in City contributions to welfare funds during that audit period, less than one-half percent, were subject to an audit. The audits that have been conducted identify serious mismanagement and make recommendations for improvement; the Comptroller’s office follows up with funds to determine whether corrective actions have been taken and occasionally conducts a follow up audit, but it has no authority or responsibility to ensure the recommendations are implemented.

CBC recommends the Office of the Comptroller, in partnership with the Office of Labor Relations (OLR) and union leadership, expand oversight of union-administered welfare funds through the following actions:

- Conduct more audits: In its oversight over all city spending, the Office of the Comptroller should give higher priority to auditing benefit funds. In the 2009 to 2017 period when 11 welfare fund audits were conducted, there were 59 audits of the Department of Parks and Recreation, despite it having roughly half the budget. Benefit fund audits should be prioritized based on risk factors including excessive administrative expenses, unnecessary reserves, or inadequate reserves.

- Enhance standards: Currently Directive #12 sets financial and operating guidelines for benefit funds. Corresponding benchmarks and indicators are needed that can trigger enforcement powers.

- Expand enforcement power: OLR, in negotiation with labor unions, should expand the Comptroller’s oversight and enforcement authority over union-administered benefit funds: current agreements allow the Comptroller to “audit and request specific information from the Benefit Funds, and describe the Funds’ underlying reporting responsibilities.”13 The Comptroller should also be able to sanction funds that fail to adhere to the guidelines laid out in Directive #12 (and the accountability standards developed in line with recommendation number 2) and have the authority to remove fund officials who fail to manage properly their members’ benefits.14

Long Term: Restructure Benefit Delivery

As previously described, smaller funds have high administrative costs and a tendency to build unnecessary reserves. Moreover, they are not able to optimize arrangements with health insurance organizations as the volume of “covered lives” involved is a major factor, and they may lack the expertise to purchase the most appropriate benefits packages.

Given that members of smaller benefit funds are disproportionately burdened by these inefficiencies, CBC makes the following recommendations to restructure how benefits are provided:

- Consolidate supplementary health care benefits under the City’s Health Insurance Plan: Because the majority of the welfare funds offer similar benefits (prescription drug, dental, and optical), it would be more efficient to consolidate the provision of these health benefits within the City’s health insurance program.

- Provide non-health related benefits through a centralized cafeteria plan: While many welfare funds offer similar benefits, there is more variability in the non-health welfare benefits offered. These benefits, while diverse, could be provided in a consolidated manner by utilizing the cafeteria plan model. Eligible employees would be entitled to choose from a list benefits with a limit on the dollar value, allowing for benefits to be tailored to an individual rather than an entire union. Annuity benefits could be integrated as one of the cafeteria plan offerings giving more members access to that benefit if they choose.

New York City’s Independent Budget Office estimates that consolidating administrative functions would produce administrative savings of $16.0 million annually.15 Consolidating the purchase of pharmaceutical and other benefits would produce savings of $98.6 and $49.3 million, respectively, for combined administrative and benefit savings of $163.8 million.16

It is anticipated that the City, in ongoing collective bargaining negotiations with labor, will seek to offset pay increases though concessions on other benefits, including contributions to benefit funds. Improving oversight and reforming the structure of benefit administration would reduce costs while maintaining benefits. This should be both the City’s and unions’ preferred option moving forward.

This policy brief is an update of the CBC report Better Benefits from our Billion Bucks: The Case for Reforming Municipal Union Welfare Funds published in August 2010.

Footnotes

- Office of the New York City Comptroller, Internal Control and Accountability Directives: Directive #12A: Municipal Labor Committee Union Employee Benefit Funds (Updated June 29, 2015), https://comptroller.nyc.gov/wp-content/uploads/documents/Directive-12A-MLC-Union-Employee-Benefit-Funds.pdf.

- The Comptroller’s office excluded 17 funds from its analysis for various reasons including: funds receive a substantial share of revenue from non-City sources, funds that would distort category averages, or funds that no longer receive City contributions.

- As of the November Modification of the Fiscal Year 2018 Budge. See: City of New York, Mayor’s Office of Management and Budget, email to Citizens Budget Commission Staff (November 29, 2017).

- Many unions operate two separate funds for their retirees and active employees. Of the 76 welfare funds, 32 service active employees, 23 are for retirees, 17 are combined, and 4 do not specify.

- The three funds included in the analysis were District Council 37, United Federation of Teachers, and the Patrolmen’s Benevolent Association. See: Courtney Wolf and Chuck Brecher, Better Benefits from our Billion Bucks: The Case for Reforming Municipal Union Welfare Funds (Citizens Budget Commission, August 2010), https://cbcny.org/research/better-benefits-our-billion-bucks.

- Office of the New York City Actuary, Summary of Other Postemployment Benefits Provided in the New York City Health Benefits Program in Accordance with GASB 74 and 75: For Fiscal Year Ended June 30, 2017 (June 2016), Appendix B, Tables 2a-2e, www1.nyc.gov/assets/actuary/downloads/pdf/OPEB_Report_FY2017.pdf.

- On occasion the City has agreed to release funds from the Health Insurance Stabilization Fund to supplement City contributions paid for out of the general fund. For example, in fiscal year 2010, there was a one-time payment of $200 per member. And in 2016, the City agreed to pay $100 per active employee and retiree to the welfare funds to help offset the increasing costs of prescription drugs. On at least one occasion a union (Local 372 DC 37) has voted to divert half of a planned 3 percent wage hike into its welfare fund after the funds solvency was threatened. See: City of New York, Office of Labor Relations, 2012-2017 Memorandum of Understanding Between The City of New York and The Patrolmen’s Benevolent Association (January 2017), p. 3, www1.nyc.gov/assets/olr/downloads/pdf/collectivebargaining/pba-nyc-moa-2012-2017.pdf; City of New York, Mayor’s Office of Management and Budget, Executive Budget for Fiscal Year 2017, Revenue Financial Plan Detail (April 2016), p. 60, www1.nyc.gov/assets/omb/downloads/pdf/exec16-rfpd.pdf; and James Harney, “Local 372 Votes to Cut Hike to Aid Benefit Fund,” The Chief-Leader (July 11, 2016), http://thechiefleader.com/news/news_of_the_week/local-votes-to-cut-hike-to-aid-benefit-fund/article_ea7be270-2764-11e6-abb9-43c39e8e7a27.html.

- Funds are categorized according to the size of the City’s contribution, whether they are insured or uninsured, and provide annuity or welfare benefits.

- Office of the New York City Comptroller, Audit Report on the Financial and Operating Practices of Social Services Employees Union Local 371 Welfare Fund (April 29, 2011), https://comptroller.nyc.gov/wp-content/uploads/documents/FL10_123A.pdf.

- Office of the New York City Comptroller, Audit Report on the Financial and Operating Practices of the Superior Officers Council Health & Welfare Fund of the New York City Police Department (September 30, 2009), https://comptroller.nyc.gov/wp-content/uploads/documents/FL09_099A.pdf.

- Office of the New York City Comptroller, Audit Report on the Financial and Operating Practices of United Probation Officers Association Welfare Fund (May 23, 2017), https://comptroller.nyc.gov/wp-content/uploads/documents/FM16_069A.pdf, and Office of the New York City Comptroller, Audit Report on the Financial and Operating Practices of the United Probation Officers Association Retirement Welfare Fund (May 23, 2017), https://comptroller.nyc.gov/wp-content/uploads/documents/FM16_070A.pdf.

- Office of the New York City Comptroller, Audit Report on the Financial and Operating Practices of the United Probation Officers Association Welfare Fund (June 30, 2009), https://comptroller.nyc.gov/wp-content/uploads/documents/FL08_076A.pdf, and Audit Report on the Financial and Operating Practices of the United Probation Officers Association Retiree Welfare Fund (June 30, 2009), https://comptroller.nyc.gov/wp-content/uploads/documents/FL08_077A.pdf.

- Office of the New York City Comptroller, Internal Control and Accountability Directives: Directive #12A: Municipal Labor Committee Union Employee Benefit Funds (Updated June 29, 2015), https://comptroller.nyc.gov/wp-content/uploads/documents/Directive-12A-MLC-Union-Employee-Benefit-Funds.pdf.

- The Comptroller’s Office would have to be resourced adequately in order expand enforcement powers as it may generate legal action.

- This estimate is based on fiscal year 2014 spending. See: City of New York, Independent Budget Office, Budget Options for New York City (March 2017), p. 25, http://www.ibo.nyc.ny.us/iboreports/budget_options_march_2017.pdf.

- CBC estimates consolidating the provision of supplemental benefits would save 20 percent of pharmaceutical benefit expenses (which are estimated to be 50 percent of all welfare fund expenditures or $492.8 million in fiscal year 2014) and an additional 10 percent of the remaining benefit expenditures. The estimated value of savings stem from the experience of the Veterans Health Administration, which realized savings estimated to be between 15 and 58 percent when it consolidated its pharmaceutical purchasing in 1995. See: United States General Accounting Office, Contract Management: Further Efforts Needed to Sustain VA’s Progress in Purchasing Medical Products and Services (June 2004), www.gao.gov/assets/250/243101.pdf; and Mariscelle M. Sales and others, “Pharmacy Benefits Management in the Veterans Health Administration: 1995 to 2003,” American Journal of Managed Care, vol. 11, no. 2 (February 2005), pp. 104-112, www.ncbi.nlm.nih.gov/pubmed/15726858.